Cash Basis vs. Accrual Basis Bookkeeping

Every Australian business eventually reaches the same crossroads. The spreadsheets become heavier. BAS reporting starts affecting cash reserves in uncomfortable ways. A bank asks for cleaner financial statements. Then the accounting method suddenly stops feeling like “just bookkeeping”.

That’s the moment cash basis vs. accrual basis bookkeeping becomes a strategic decision instead of an admin task.

In Australia, the choice directly affects taxable income, GST timing, compliance obligations, financing opportunities, and the accuracy of financial reporting. The Australian Taxation Office (ATO), Australian Accounting Standards Board (AASB), and ASIC all influence how businesses report revenue and expenses across each reporting period.

Here’s the practical difference:

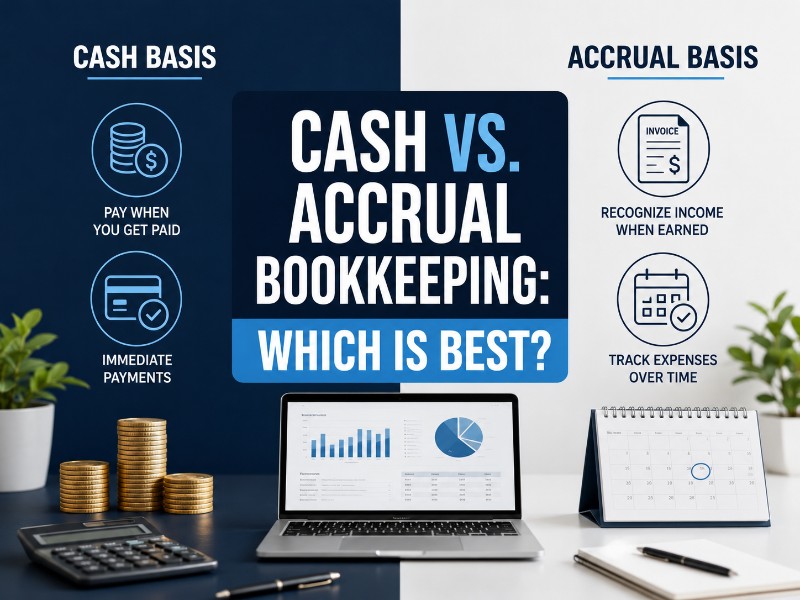

- Cash basis accounting Australia records transactions when money changes hands.

- Accrual accounting Australia records transactions when revenue is earned or expenses are incurred.

Simple on paper. Far more complicated in practice.

A growing e-commerce brand using Shopify might look profitable on a cash basis during Christmas trading while carrying massive unpaid supplier invoices underneath. Meanwhile, a consulting company operating on accrual accounting could appear cash-poor despite strong long-term contract revenue.

That disconnect matters. Especially once lenders, investors, or external auditors start examining financial statements closely.

What Is Cash Basis Bookkeeping?

Cash basis bookkeeping records income when cash receipts arrive and expenses when cash payments leave the business account.

No invoice timing complications. No accounts receivable adjustments. No accrued expenses sitting quietly in the background.

For many Australian sole traders and micro businesses, that simplicity is the entire appeal.

How the Cash Accounting Method Works

Under the cash accounting method, revenue recognition happens only after payment lands in the bank. Expenses appear only after payment occurs.

A freelance designer issuing a $6,000 invoice in June but receiving payment in July reports the income in July under cash basis bookkeeping.

The same principle applies to expenses.

This approach creates simplified record-keeping and often gives smaller businesses a clearer view of immediate liquidity position. In practice, many operators care more about “money in the account today” than theoretical profitability.

The ATO permits eligible businesses to use cash basis GST Australia reporting if turnover stays below the GST turnover threshold. BAS reporting under the cash method means GST on receipts gets reported only after customer payment arrives.

Platforms like Xero have made small business cash accounting dramatically easier over the last decade. Automated bank feeds now handle much of the heavy lifting.

Still, cash accounting has blind spots.

Profit visibility becomes distorted once unpaid invoices or inventory levels increase. That’s usually the point where growing businesses begin feeling friction.

What Is Accrual Basis Bookkeeping?

Accrual bookkeeping records revenue when earned and expenses when incurred, regardless of payment timing.

This system aligns with the expense matching principle and forms the foundation of most Australian financial reporting standards.

Why Accrual Accounting Dominates Corporate Reporting

Under the accrual accounting method, businesses recognise economic activity when it happens.

Not when cash moves.

If a Melbourne construction company completes a project milestone in May but receives payment in August, the revenue still appears in May financial statements under accrual bookkeeping Australia standards.

Likewise, accrued expenses appear before payment occurs.

That distinction creates more accurate financial statements because revenue recognition and expense allocation align within the same reporting period.

Medium and large Australian companies frequently rely on accrual accounting because the Corporations Act 2001, ASIC requirements, and AASB standards generally expect it. IFRS principles also operate primarily through accrual frameworks.

Key accrual accounting components include:

- Accounts receivable

- Accounts payable

- Deferred revenue

- Accrued expenses

- Balance sheet adjustments

Software systems like MYOB and enterprise ERP platforms handle these adjustments automatically now, although the interpretation still requires experience.

And honestly, this is where many businesses underestimate complexity. Accrual accounting delivers stronger financial accuracy, but it also exposes operational weaknesses faster.

Late-paying customers suddenly become visible. Inventory problems become impossible to ignore. Margins stop hiding behind temporary cash surges.

Key Differences: Cash Basis vs. Accrual Basis Bookkeeping

The difference between cash and accrual accounting goes far beyond bookkeeping preferences.

It changes how the business appears to lenders, investors, tax authorities, and even internal management teams.

Comparison Table: Cash vs Accrual Bookkeeping Australia

| Area | Cash Basis Bookkeeping | Accrual Basis Bookkeeping |

|---|---|---|

| Revenue recognition | Recorded when cash is received | Recorded when earned |

| Expense recognition | Recorded when paid | Recorded when incurred |

| GST reporting | GST on receipts collected | GST on invoices issued |

| Profit visibility | Focuses on cash movement | Focuses on business performance |

| Balance Sheet accuracy | Limited visibility | Full financial position shown |

| Inventory handling | Often less reliable | More accurate inventory valuation |

| Compliance suitability | Smaller Australian SMEs | Medium and large entities |

| Financing readiness | Weaker for lenders | Stronger for investors and banks |

| Administrative complexity | Lower | Higher |

| Strategic forecasting | Limited | Advanced financial modelling possible |

A practical observation tends to emerge after reviewing hundreds of Australian SME financial reports: cash accounting feels comfortable early on, but accrual accounting scales better once credit sales, payroll growth, or inventory complexity increase.

That transition point often arrives sooner than expected.

Tax Implications in Australia

Tax timing changes significantly depending on the bookkeeping method.

And this is where businesses occasionally drift into compliance risk without realising it.

GST Reporting Differences

Under GST cash vs accrual Australia rules:

- Cash basis businesses report GST after payment receipt.

- Accrual basis businesses report GST when invoices are issued.

That timing difference directly affects BAS lodgement obligations and short-term cash flow pressure.

A retailer using accrual accounting may owe output tax before customer payment arrives. During slower economic periods, that gap can create serious working capital stress.

On the other hand, accrual reporting provides cleaner visibility into assessable income and future liabilities.

Income Tax Timing

Taxable income timing also shifts.

Under cash accounting ATO rules, unpaid customer invoices generally don’t trigger immediate tax consequences. Under accrual accounting, earned revenue typically becomes assessable income even before collection.

PAYG instalments, input tax credits, and BAS cash method elections all depend on accurate classification.

Tax agents regularly encounter businesses mixing methods unintentionally. That creates reconciliation issues, especially during software migrations or rapid growth phases.

The ATO pays close attention to consistency.

Financial Reporting and Compliance Requirements

Once businesses grow beyond certain thresholds, accrual accounting becomes less optional.

That’s the reality across Australian corporate reporting.

When Accrual Accounting Becomes Necessary

Companies regulated under the Corporations Act 2001 often require accrual-based reporting to satisfy ASIC and AASB standards.

This includes preparation of:

- General purpose financial statements

- Profit and Loss Statements

- Balance Sheets

- Audit-ready reporting packages

External auditors also expect strong audit trail documentation under accrual systems.

Australian banks reviewing commercial lending applications usually prefer accrual-based financial transparency because it reveals liabilities, revenue stability, and working capital more accurately.

Cash basis reporting can sometimes obscure financial weakness. Lenders know that.

Investor-backed companies, especially those engaging Australian venture capital firms, almost always transition toward accrual reporting before significant funding rounds.

Strategic Decision-Making and Growth Planning

Bookkeeping methods influence strategic planning more than many founders expect.

Especially once turnover approaches AUD $10 million.

Why Accrual Accounting Supports Growth

Accrual accounting supports:

- EBITDA analysis

- Cash flow projections

- Financial modelling

- Capital raising

- Performance metrics tracking

Major lenders like Commonwealth Bank, Westpac, ANZ, and NAB often examine accrual-adjusted earnings before approving larger commercial finance applications.

That’s because accrual reporting shows recurring revenue trends more clearly.

Cash accounting, meanwhile, excels at operational survival visibility. Hospitality venues, trades businesses, and seasonal operators frequently prefer immediate cash flow interpretation because payroll pressure is constant.

Now, here’s the interesting part.

Many successful Australian businesses actually monitor both perspectives internally. Accrual reporting handles compliance and strategy while cash reporting guides day-to-day liquidity decisions.

That hybrid mindset tends to produce stronger financial discipline.

Industry-Specific Considerations in Australia

Different industries naturally lean toward different bookkeeping methods.

The business model often decides first.

Construction Industry

Construction businesses dealing with progress billing and long-term contracts generally benefit from accrual accounting.

Contract revenue recognition becomes critical once projects stretch across multiple reporting periods.

Retail and Hospitality

Retail Trade Australia businesses often rely heavily on cash flow monitoring during Christmas trading periods.

Inventory turnover moves quickly. Supplier payments stack up fast. Cash visibility becomes essential.

Professional Services

Consultancies and legal firms using extended billing cycles usually adopt accrual bookkeeping Australia systems to track accounts receivable accurately.

Otherwise profitability becomes misleading.

Agriculture

Agricultural businesses experience seasonal cash flow volatility tied to harvest timing and commodity pricing.

Cash basis accounting can simplify operations during unpredictable revenue cycles.

E-commerce

Subscription revenue and online platform sales through Shopify or Square frequently push businesses toward accrual accounting because deferred revenue tracking matters.

Especially once scale arrives.

Transitioning from Cash to Accrual in Australia

Switching methods sounds straightforward. In practice, the transition can get messy surprisingly fast.

Key Transition Steps

Moving from cash to accrual accounting usually involves:

- Recording accounts receivable

- Recording accounts payable

- Adjusting opening balances

- Creating journal entries

- Reconfiguring accounting system settings

- Managing GST adjustments

- Completing reconciliation processes

Xero and MYOB both support conversion workflows, although comparative reporting issues occasionally appear during migration periods.

Businesses changing methods may also need to notify the ATO depending on reporting structure and GST treatment.

CA ANZ professionals and BAS agents frequently assist with transition planning because even small errors can distort taxable income across multiple periods.

And unfortunately, those mistakes tend to surface during audits or financing applications rather than immediately.

Choosing the Right Method for Your Australian Business

The best accounting method Australia businesses choose depends on operational complexity, growth plans, and compliance exposure.

No single method fits every business stage.

Cash Basis Often Fits Businesses That:

- Operate as sole traders

- Maintain low turnover

- Primarily receive immediate payment

- Need simplified bookkeeping methods Australia compliance

- Focus heavily on short-term liquidity

Accrual Basis Often Fits Businesses That:

- Carry inventory

- Offer credit terms

- Seek investment funding

- Require ASIC-compliant reporting

- Need advanced forecasting capability

- Plan aggressive scaling

The turnover test also matters.

Once businesses expand into larger staffing structures, financing arrangements, or interstate operations, accrual accounting usually becomes more practical despite the added compliance burden.

Professional advisory support from accountants, CA ANZ advisers, or tax agents often becomes worthwhile at that stage because strategic alignment matters more than bookkeeping simplicity alone.

Conclusion

Cash basis vs. accrual basis bookkeeping affects far more than accounting entries.

It shapes tax liability timing, financial visibility, compliance obligations, funding readiness, and long-term scalability.

Cash basis accounting Australia frameworks provide clarity around immediate liquidity and simplified reporting. Accrual accounting Australia systems deliver deeper financial accuracy, stronger forecasting capability, and better alignment with AASB reporting standards.

Most Australian SMEs begin with cash accounting because operations stay relatively simple early on. Growth changes that equation.

Eventually, unpaid invoices, inventory movement, financing demands, and reporting obligations create pressure for more sophisticated financial reporting.

That transition tends to happen gradually… until suddenly it doesn’t.

Businesses that understand both methods early usually make cleaner decisions later. And in Australia’s increasingly compliance-driven environment, that financial clarity becomes a competitive advantage rather than just an accounting preference.